xxx

‘found worrying or nasty in some way’

From Making Britain the safest place in the world to be online – GOV.UK

Yes, well I find things like this every single day on the internet. For example, I am very worried about

A library of snippets

xxx

‘found worrying or nasty in some way’

From Making Britain the safest place in the world to be online – GOV.UK

Yes, well I find things like this every single day on the internet. For example, I am very worried about

xxx

While the implausible nature of the $9 billion price tag may have been a red flag to human traders, Apple did briefly see its stock rise to $158 before settling back down to around $156, raising the possibility that some algos were fooled.

From Fake news: Dow Jones blames technical error for headlines claiming…

xxx

Perhaps the universe was telling me something, because it seems to me beyond coincidence that I don’t remember hearing the word “homophily” before and yet I’ve just come across it twice in the same day: once when listening to historian Niall Ferguson on the BBC’s Today programme while in the shower and then again a couple of hours later while reading Geoff Mulgan’s new book “Big Mind” on the couch. Homophily means the tendency of people (e.g., me) to tend to congregate online with people who think the same as they do (e.g., the Chancellor of the Exchequer is very probably insane) but worse still in the new online world, also view only “news” (fake or real) that reinforces their position.

We will come back to homophily in a moment.

Geoff’s thesis is that the “collective intelligence” formed from groups of people connected together online functions according to new dynamics. Now, while he notes early on that a more networked world does not automatically means a higher IQ world (in fact, as far as I can see, the general level of idiocy has increased substantially since the early days of the the telegraph and the bulletin board), and that “shared thought is not only knowledge but delusions, illusions and fantasies”, I’m not sure that Snapchat boosts either individual or collective IQs.

Hence I began with caution, and about two thirds of the way through the book I was caught in a terrible English dilemma. I’ve known the author for a long time and admired his work with Demos and NESTA. But I wasn’t enjoying the book and didn’t feel I was getting anything from it. So how could I say that politely?

Luckily I carried on reading and I realised that the first two-thirds of the book is not for people like me who spend their entire lives on LinkedIn and Twitter but for politicians and policymakers who have only the vaguest idea of what these new technologies are and just how different these new dynamics of the collective that they have created is from the collection of individuals that they are used to dealing with.

It’s the last third of the book where Geoff gets into the tough questions. I’d not heard of the “folk theory of democracy” (i.e., that the people are wise and come to the right answer) before but I can say with certainty that it is doomed with the masses so easily subverted through Facebook adverts and clickbait headlines. While it is appealing to hope that new technology is the answer, a means to rejuvenate democracy, I’m not sure. As the author notes, crowds are good at ideas, not judgements.

Do we then give decision making to an elite? Maybe, but the experts aren’t always right even when they are more connected than ever before. I strongly agree with the author’s view that “expertise can entrap”, or to put it another way, foxes make better predictions than hedgehogs, but we don’t seem to be rummaging through the dustbins of knowledge to pick out the good stuff at all. The example the author uses illustrates this rather well: we have more data about health and diet and nutrition than ever before, yet we have an epidemic of obesity. More data does not mean wisdom.

Which leads me to my suspicion is that it isn’t networking people together that is going to help, but networking people with artificial intelligences. As Geoff himself points out, technologies can effectively perform many of the elements of collective intelligence. He references a a Hong Kong investment firm has already invited an AI to join its board and given it the same vote as human board member.

A cabinet of ZX Spectrums could hardly do worse than the flesh and blood version. I laughed out loud when I saw “government is collective intelligence” since there’s precious little evidence of such (“government is muddling through” is more the British way). Geoff has had access to government decision-making process that I have not, so how accurate his characterisation is I can’t say. He certainly right when he says that companies pretend to operate with collective intelligence but actually go by gut feeling rules of thumb (as memorably described in one of my favourite books from last year “Chaos Monkeys”).

Geoff puts forward an interesting thesis but doesn’t completely convince with it. At the end of the book, I was left unsure whether he thinks that the online collective multi-intelligence of the connected crowd is something to be harnessed, managed or avoided at all costs.

xxx

“Zero-knowledge proofs are one of the biggest inventions in the last two decades in cryptography,” said Emin Gun Sirer, an associate professor of computer science at Cornell University. It “will allow a slew of applications we can’t even imagine right now.”

From ‘Mind-Boggling’ Math Could Make Blockchain Work for Wall Street – Bloomberg

xxx

xxx

According to RBA estimates, the merchant will pay an average of about 0.55 per cent of the transaction’s value in a “merchant service fee” to their bank when the payment goes through the credit card network. But if it goes through the eftpos (CHQ or SAV) system, this drops to 0.15 per cent.

xxx

As I’ve written many times (e.g., here), it is difficult to overestimate the impact of artificial intelligence (AI) on the financial services industry. As Wired magazine said, “it is no surprise that AI tops the list of potentially disruptive technologies”. With Forrester further forecasting that a quarter of financial sector jobs will be “impacted” by AI before 2020, there’s an urgent need to develop strategies in this. It is because the need is so urgent that I was delighted to be asked to give a keynote at the Digital Jersey AI Retreat in September, an event was put together by my good friends at Digital Jersey (where I am advisor to the board) working with Cognitive Finance. They did a great job of bringing together a spectrum of both subject matter experts and informed commentators to cover a wide variety of issues and provide a great platform for learning.

In “Radical Technologies”, Adam Greenfield wrote of the advance of automation that many of us (me included, by the way) cling to the hope that “there are some creative tasks that computers will simply never be able to peform”. I have no evidence that financial services regulation will be one of those tasks, so in my talk I suggested AI will be the most important “regtech” of all and made a few suggestions as to how regulators can plan to use the technology to create a better (that is faster, cheaper and more transparent) financial services sector.

Regulation, however, was only one the topics discussed in a fascinating couple of days of talks, discussions and case studies. The surprise for me was that there was a lot of discussion about ethics, and how to incorporate ethics into the decision-making processes of AI systems so that they can be audible and accountable. I hadn’t spent too much time thinking about this before, but I was certainly left with the impression that this might be one of the more difficult problems to address and talking with very well-informed experts. Although I must say that the most surprising discussion of the event that I was personally involved in took a very different tack: whether AIs employed in the service of financial institutions should come under the HR department or the IT department!

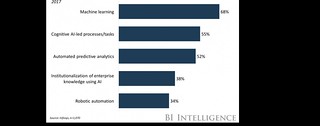

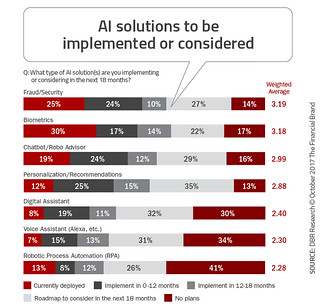

OK. So banks are going to be disrupted by AI. But where to start? I happened to be reading Call Credit’s interesting white paper “Credit, Fraud and Risk in the Age of Machines”. Their data scientists explore the use of machine learning in credit risk and fraud prevention. It’s that latter category that interests me most at the moment simply because fraud is so out of control, so I began to wonder whether this new technology is having any impact. Are Call Credit right to be optimistic about machine learning? The answer seems to be that they are, and that there may be light at the end of the tunnel. If we look at what AI is being deployed in the banking sector and what is it being used for, we see this optimistic reinforced.

Let’s look in more detail. First of all, AI is an umbrella term so we need to be a little more specific. The most recent figures seem to indicate that the technology of machine learning is the main area of investment in banking. This is not surprising, because machine learning thrives when fed wast quantities of structured data. Banks have this in spades but have historically found it difficult to extract wisdom from it.

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

What are they using these machine learning systems for? Well, fraud does indeed seem to be the main business case with identification and authentication (including the use of biometrics) the highest priorities. Chatbots, robo-advisors and digital assistants are all fun, but in terms of making an impact on the bottom line, doing something about fraud beats everything else.

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

Hence my optimistic interpretation. Identity is a mess, but we may be able to use AI to begin to mitigate some of the effects of this in the banking sector. Dave Webber, Director of Concept Management at Call Credit, sums it up nicely in their white paper by saying that “machine learning can help businesses make decisions by looking at data patterns… then looking for anomalies that indicate something isn’t right”. AI is good at this sort of pattern recognition and, I think, so much better at it than we are that it might even outsmart the fraudsters.

xxx

Officers initially confiscated his passport before Ali changed his name by deed poll and applied for a new one, flying to Dubai two days before he was to be tried for possessing a quantity of bullets.

From Arab driver filmed himself in his Porsche going 180mph | Daily Mail Online

xxx

snippet

To maintain their cover, undercover detectives were posting and sharing abuse material on Childs Play. Other users continued to post and view images while the site was under police control.

[From

Australian police sting brings down paedophile forum on dark web | Society | The Guardian

]

snippet

xxx

Chancellor Philip Hammond has announced a new National Productivity Investment Fund of £23 billion to be spent on innovation and infrastructure over next five years.

From Chancellor announces £23bn Productivity Investment Fund – ITV News

Since this announcement productivity has collapsed still further.

xxx

The accumulating evidence on economic growth, meanwhile, has become damning. Between July and September 2016, India’s GDP grew 7.53 percent. Between January and March 2017 it grew 5.72 percent. Former head of the Reserve Bank of India Raghuram Rajan, now returned to the University of Chicago, links the drop to demonetization: “Let us not mince words about it — GDP has suffered. The estimates I have seen range from 1 to 2 percentage points, and that’s a lot of money — over Rs2 lakh crore [i.e. trillion] and maybe approaching Rs2.5 lakh crore.” Kaul adds that GDP does not well capture the size of the informal cash sector, where the losses from demonetization were greatest.

From India’s Failed Demonetization Program and Its Retreating Economic Defenders – Alt-M

So why does the Bank of England think that getting rid of paper cash will boost the economy when the figures from India clearly show it didn’t. The answer, of course, relates to the stage of development of the economy. In England, there are ready alternatives to cash that almost everyone already uses. Contactless cards and mobile phones mean that if all the ATMs in England gave up the ghost tomorrow, it wouldn’t really matter. Yes, there are some unbanked people and, as I have long argued, we should be providing digital financial services that are appropriate to them (not forcing them to use bank accounts) so that they can use electronic alternatives. Having been involved in projects to do just this (e.g., mobile money accounts for “universal credit” recipients and services delivered via digital TV to the housebound) I can honestly say that I do not find insurmountable problems.

While the India has taken great strides (the introduction of “payment banks”)

xxx

“‘There were a lot of people who came and clicked photos (of the sign) but apart from that no transactions,’”

Bitcoin accepted here: The tiny family restaurant in India that’s embraced virtual currency — Quartz

xxx