The US Treasury’s report on “Nonbank Financials, Fintech, and Innovation” prepared in response to Mr. Trump’s “Executive Order 13772 on Core Principles for Regulating the United States Financial System” is, I have to say, most comprehensive. It covers a great many aspects of the financial services market, as you would imagine, and covers a few specific areas that I think are worth detailed consideration and due some real innovation. One of them is digital identity.

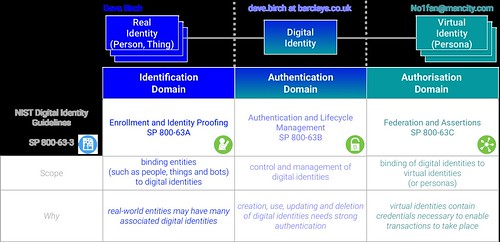

The Treasury report says that digital identity systems may rely on various types of technology but generally involve two essential components: (1) identity proofing, enrollment, and credentialing; and (2) authentication. It then goes on to say that they may also involve (3) federation, which is optional, but allows identity to be portable.

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

Indeed. This is a reasonable way to think about the problem. I presented this view at the MobeyForum Members’ Meeting in Paris, showing how these three components are used in our “three domain identity” or “3DID” model for digital identity that I have written about before. Here’s the model, along with the US National Institute of Standards and Technology (NIST) draft standards, in a picture from that presentation.

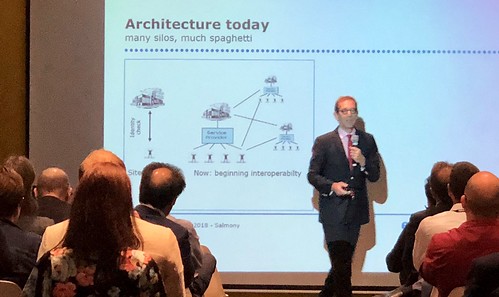

Of course I don’t regard the federation as optional because I’m not really interested in identity solutions that work only for the issuer. What I think the mass market wants is identities that individuals can choose to use in as many or as few places as they like. A Barclays identity that I can only use to log in to Barclays is one thing, whereas a Barclays identity that I can use to log in to all sorts of places in much more desirable. Michael Salmony made this point quite well in his presentation to MobeyForum event, making the point (similar to mine) that existing digital identity efforts were not really producing the results that we want.

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

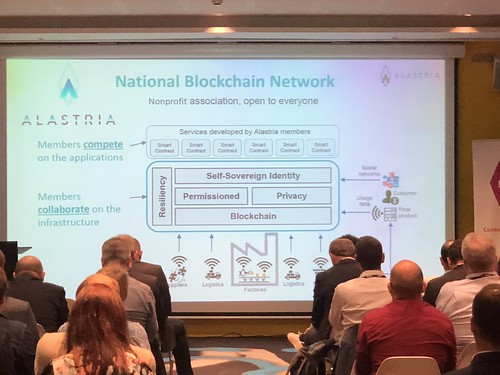

One point that Michael made

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

Xxx