xxx

The current AML/CFT model appears almost completely ineffective in disrupting illicit finances and serious crime.

From Uncomfortable truths? ML=BS and AML= BS2 | Journal of Financial Crime | Vol 25, No 2.

xxx

A library of snippets

xxx

The current AML/CFT model appears almost completely ineffective in disrupting illicit finances and serious crime.

From Uncomfortable truths? ML=BS and AML= BS2 | Journal of Financial Crime | Vol 25, No 2.

xxx

xxx

The trainee member of staff with the London Ambulance Service flunked his paramedic exams but carried out “unauthorised” responses to 999 calls for several weeks.

It is understood he was able to pose as a qualified paramedic by infiltrating an internal computer system used by emergency crews while they are on duty.

From ‘Fake’ paramedic treats more than 100 patients in London before being discovered.

xxx

xxx

While Zelle is both free to the user and instantaneous, it costs the participating bank between $0.50 to $0.75 per transaction. So as Zelle’s transaction volume increases, so will each bank’s costs.

From Bank Director :: Zelle Costs Bankers Money, Venmo Can Make Bankers Money.

But surely as the volume rises, the per transaction costs (that go to fund the network) will go down.

I’m always in awe of the inventiveness of fraudsters. Consider the recent example of the maps mountebanks who used Google Maps to trick unsuspecting Indian customers into giving up personal information. The Google Maps app lets users edit and update listings, so the fraudsters are changing banks’ phone numbers to their own!

xxx

Universal black box adoption has two appealing features for society. First, it is fair. Instead of drivers being lumped into broad-brush buckets, they can pay a premium that closer reflects the fair price for their unique probability of making a claim. Unlike in markets such as healthcare, the individual probability of driving incidents is less determined by inherent or genetic characteristics. The most common car insurance claims are rear-end collisions, which can often be avoided with more attention paid to speed, spacing and road conditions.

Second, widespread use of black boxes is also likely to lead to higher quality driving and fewer fatalities. The WHO estimates that there are around 1.25 million annual deaths due to road traffic accidents across the globe. How many lives would be saved if drivers knew they could save large amounts of money by paying more attention to their driving habits?

From Car insurance telematics: why the black box should become more transparent | Bank Underground.

xxx

xxx

“While we have had RealMe in New Zealand for many years it is time to relook at whether a single centralised ID is the best approach in a world where people want ease of use and mobility at the same time as privacy and security.

From Kiwis starting to embrace digital identity – NZTech | Voxy.co.nz.

xxx

xxx

A Japanese company has developed an artificial intelligence-powered automated teller machine to prevent fraudulent money transfers, the first of its kind in the country.

The system, which can recognize the appearance and movement of ATM users through an embedded camera, aims to help prevent crimes in which scammers guide elderly victims over the phone to transfer money by making them believe they will be refunded a higher amount.

xxx

xxx

A new study from Juniper Research has found that annual online payment fraud losses from eCommerce, airline ticketing, money transfer and banking services, will reach $48 billion by 2023; up from the $22 billion in losses projected for 2018.

From Losses from Online Payment Fraud to More than Double by 2023.

xxx

What an interesting experience the first Money2020 in China was. It was held in Hangzhou, the home of AliPay, and I was delighted to have been invited along to share some of our experiences in the payments and to learn first hand about the Chinese approach to the sector.

Money2020 China gets underway

The event was well-staged and with simultaneous translation from Chinese it provided an opportunity to hear about the wide variety of fintech activities in China. It was, as you might imagine, very different from the Las Vegas event last month. There was no discussion of cryptocurrency because of the Chinese regulatory context and while I did see one presentation on the use of digital signatures in smart contracts, there was little discussion of blockchain and related technologies.

Ron Kalifa talking about value-added merchant services

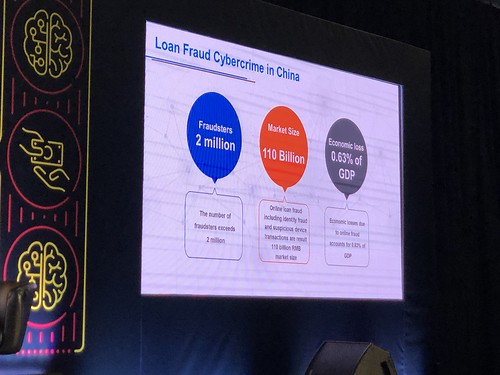

I particularly enjoyed Worldpay vice-chairman Ron Kalifa’s fireside chat (in which he said that people were underestimating the impact of open banking) and presentation of their annual world payments report. To a payments nerd like me this was a great opportunity to look at key trends in payments on a country-by-country basis and try to work out which trends are relevant to our clients around the world as they formulate strategies for the always-on, mobile-centric, open-banking future. Key to these strategies is, of course, security and so I always pay attention to the big picture presentations around fraud. In China, these have scary numbers attached to them, but you have to take into account the size of the Chinese economy (I think the Chinese cybercrime losses are lower than in many other countries).

Real, and scary, fraud numbers

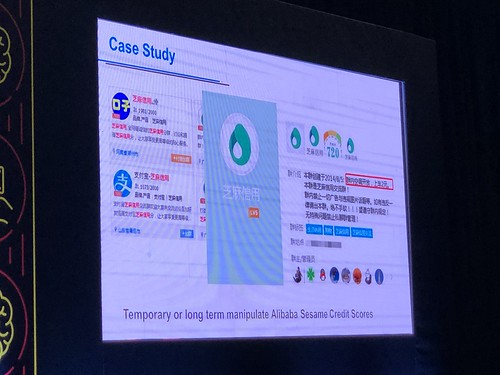

Given the widespread use of scores of one form or another to determine trustworthiness it is no coincidence that China sees a rise in frauds relating to the manipulation of these scores. Without commenting on the benefits or otherwise of such models (most Brits, myself included, can only think of Black Mirror when social scores are discussed) it is worth making the point that preventing “gaming” of these scores while preserving individual privacy means dealing with paradoxes that might well be resolved through the use of cryptographic techniques that have no conventional analogues and are therefore difficult for policymakers to bear in mind.

Reputation fraud in action

Most of what I found thought-provoking, both in the presentations and the water cooler discussions, was to do with business models rather than new technologies. The new business models emerging in a regulated, platform-centric, dynamic market are what we should be studying. We might choose to implement some of these models in a slightly different way taking into account the varying cultural norms around security and privacy, but the idea of separating payments from banking and then turning payments into platforms, and then using these platforms to acquire customers at scale for other businesses is certainly very interesting.

These new models, of course, centre on data and value-adding using that data. When people pay for everything with their mobile phone, they lay down a seam of data that is waiting to be mined. Despite this, the convenience of the mobile-centre platforms is so great that people are clearly willing to put privacy concerns to one side. I chaired a great session on privacy with CashShield, Symphony and eCreditPal with, I think, gave out a very comforting message: if you build services with privacy in the first place, then actually complying with GDPR and other global regulations is actually not that much of a problem.

One more thing that struck me about the context for these developments that it seems to me that China is making its e-money regulation more like the EU’s. With an EU electronic money licence, the organisations holding the funds must keep them in Tier 1 capital and are not allowed to gamble the customer’s money, whereas in China there was no such restriction. Now the People’s Bank has said that from January 2019 the Chinese operators will have to hold a 100% reserve in non-interest bearing deposits at a commercial banks, a decision that will likely cost the main players (Tencent and Alipay) a billion dollars or so in revenue.

It was interesting spend a few days inside the mobile-centric, QR-everywhere, always-on, app and pay world of the future and picking up some useful lessons for our clients. A very interesting week.

I had the good fortune to attend the Australian Payment Summit 2018 in Sydney this year, chairing the panel on Digital Currency and giving the first day closing keynote on the impact of artificial intelligence in the transaction space (I was developing the “where are the customers’ bots” theme).

Naturally, one of the areas that I wanted to find out about was digital identity. As in many other countries, Australia is trying to deal with a complex mixture of requirements, goals and constraints for some form of digital identity infrastructure and it is far from clear what is going to happen. In the lead up to the event, the CTO of Westpac was quoted saying that “if you are going to move to a more open data-connected world, which we clearly are… you have to solve the problem of digital identity”. Well, yes. I agree 100%.

But how?

There is scepticism about a government solution. The Department of Home Affairs is looking at a single national digital identifier, which I am not sure is the right way forward since identity, as far as I am concerned, should be a menu. A recent report from Australian Strategic Policy Institute (a think tank) cautioned that an attempt to create some sort of digital identity could end up as “a repeat of the failed attempt to roll out the Australia Card” unless the government builds in privacy which, naturally, I agree with. So perhaps it is better to look to the private sector.

With a private sector solution, my preferred first step, of course, is to have regulated financial institutions do it. In Australia,this is indeed what is happening. Their approach is to have the Australian Payment Network (AusPayNet) tackle the problem under the auspices of the Australian Payments Council and they have been doing an interesting experiment in “agile” development to begin to explore what might be practical in the mass market, but it is still not clear how the banks will work together to deliver a mass-market solution that will be the platform that a modern economy needs. And, it turns out, I am not the only one.

//embedr.flickr.com/assets/client-code.js

//embedr.flickr.com/assets/client-code.js

In his keynote speech at the Summit the Governor of the Reserve Bank of Australia (RBA), Philip Lowe, said that digital identity is likely to become increasingly important as more and more activity takes place online and went on to say that the RBA is “highly supportive” of industry collaboration on this issue and views it as important that substantive progress is made. During the Q&A session he said (I paraphrase) “we all agree that something must done, but we can’t agree on what is it” and that the “institutions will need to compromise in the national interest”. I think these are very interesting (and very insightful) remarks.

This led me to