What an interesting experience the first Money2020 in China was. It was held in Hangzhou, the home of AliPay, and I was delighted to have been invited along to share some of our experiences in the payments and to learn first hand about the Chinese approach to the sector.

Money2020 China gets underway

The event was well-staged and with simultaneous translation from Chinese it provided an opportunity to hear about the wide variety of fintech activities in China. It was, as you might imagine, very different from the Las Vegas event last month. There was no discussion of cryptocurrency because of the Chinese regulatory context and while I did see one presentation on the use of digital signatures in smart contracts, there was little discussion of blockchain and related technologies.

Ron Kalifa talking about value-added merchant services

I particularly enjoyed Worldpay vice-chairman Ron Kalifa’s fireside chat (in which he said that people were underestimating the impact of open banking) and presentation of their annual world payments report. To a payments nerd like me this was a great opportunity to look at key trends in payments on a country-by-country basis and try to work out which trends are relevant to our clients around the world as they formulate strategies for the always-on, mobile-centric, open-banking future. Key to these strategies is, of course, security and so I always pay attention to the big picture presentations around fraud. In China, these have scary numbers attached to them, but you have to take into account the size of the Chinese economy (I think the Chinese cybercrime losses are lower than in many other countries).

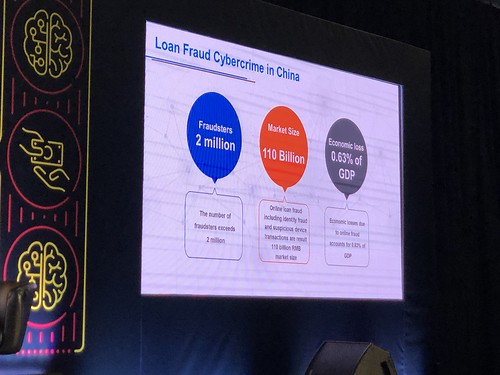

Real, and scary, fraud numbers

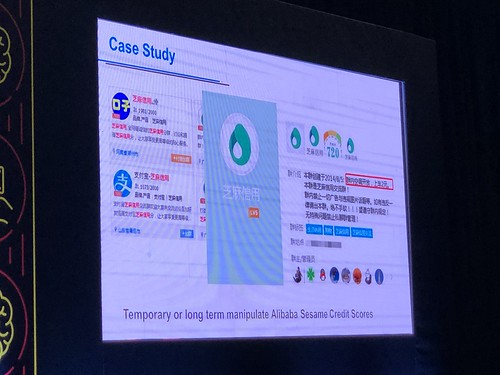

Given the widespread use of scores of one form or another to determine trustworthiness it is no coincidence that China sees a rise in frauds relating to the manipulation of these scores. Without commenting on the benefits or otherwise of such models (most Brits, myself included, can only think of Black Mirror when social scores are discussed) it is worth making the point that preventing “gaming” of these scores while preserving individual privacy means dealing with paradoxes that might well be resolved through the use of cryptographic techniques that have no conventional analogues and are therefore difficult for policymakers to bear in mind.

Reputation fraud in action

Most of what I found thought-provoking, both in the presentations and the water cooler discussions, was to do with business models rather than new technologies. The new business models emerging in a regulated, platform-centric, dynamic market are what we should be studying. We might choose to implement some of these models in a slightly different way taking into account the varying cultural norms around security and privacy, but the idea of separating payments from banking and then turning payments into platforms, and then using these platforms to acquire customers at scale for other businesses is certainly very interesting.

These new models, of course, centre on data and value-adding using that data. When people pay for everything with their mobile phone, they lay down a seam of data that is waiting to be mined. Despite this, the convenience of the mobile-centre platforms is so great that people are clearly willing to put privacy concerns to one side. I chaired a great session on privacy with CashShield, Symphony and eCreditPal with, I think, gave out a very comforting message: if you build services with privacy in the first place, then actually complying with GDPR and other global regulations is actually not that much of a problem.

One more thing that struck me about the context for these developments that it seems to me that China is making its e-money regulation more like the EU’s. With an EU electronic money licence, the organisations holding the funds must keep them in Tier 1 capital and are not allowed to gamble the customer’s money, whereas in China there was no such restriction. Now the People’s Bank has said that from January 2019 the Chinese operators will have to hold a 100% reserve in non-interest bearing deposits at a commercial banks, a decision that will likely cost the main players (Tencent and Alipay) a billion dollars or so in revenue.

It was interesting spend a few days inside the mobile-centric, QR-everywhere, always-on, app and pay world of the future and picking up some useful lessons for our clients. A very interesting week.